A Lot Happened. Here's What Actually Matters.

- Joshi Koneru

- Feb 24

- 3 min read

Good news, mixed signals, and one thing worth watching. That's the economy in a sentence right now. Growth is surprising to the upside, inflation is headed in the right direction, and unemployment is low by any reasonable measure. But the job market has some nuance beneath the surface that's worth understanding before you decide how you feel about all of it.

The job market is at a turning point

One useful way to read the job market is to compare how many people are looking for work against how many openings exist. For a while after the pandemic, employers were desperate — at the peak in 2022, there were two open jobs for every job seeker. That gap has closed. Today there are roughly 7.4 million unemployed Americans chasing 6.5 million openings, the fewest available positions since late 2020.

The monthly numbers still look decent — January added 130,000 jobs, nearly double what economists expected, and unemployment ticked down to 4.3%. But zoom out and the picture gets more interesting: total job creation for all of 2025 came in at just 181,000, about 15,000 a month, the weakest annual figure since 2020. Unemployment has stayed low partly because fewer people are looking for work at all — an aging population and slower immigration mean both the supply of workers and the demand for them are cooling at the same time. Worth knowing, even if it's not a reason to lose sleep.

Inflation and the broader economy

Jobs matter because they drive consumer spending — and consumer spending is more than two-thirds of the U.S. economy. On the inflation front, the news is genuinely good: prices rose just 2.4% over the past year, and core inflation — which strips out food and energy — has slowed to 2.5%, the lowest in nearly five years. That puts the Federal Reserve close to its 2% target. Prices haven't fallen, but the fact that they're rising more slowly is a win for both your household budget and your portfolio.

Oil, Iran, and the Long View

Geopolitical tensions in the Middle East have pushed oil prices up about $10 a barrel this year — though prices remain low by historical standards. The bigger risk to watch is the Strait of Hormuz, which carries roughly a third of the world's oil supply; any disruption there could spike energy prices and add to inflation. That said, markets have historically shaken off geopolitical volatility once the dust settles, and staying the course has consistently been the right call for long-term investors.

Supreme Court ruling and Tariffs

The Supreme Court's 6-3 ruling striking down the broad IEEPA tariffs removes one of the bigger sources of market uncertainty from the past year. Most of the sweeping tariffs — including the "reciprocal tariffs" from last April — are out, though steel, aluminum, and auto tariffs remain. The White House may look for other legal avenues to reimpose them, so this likely isn't the final word on trade policy. For investors, the practical takeaway is that tariff-driven volatility may ease, but corporate earnings and economic growth — not trade headlines — are what drive long-term portfolio performance.

What this means for your portfolio

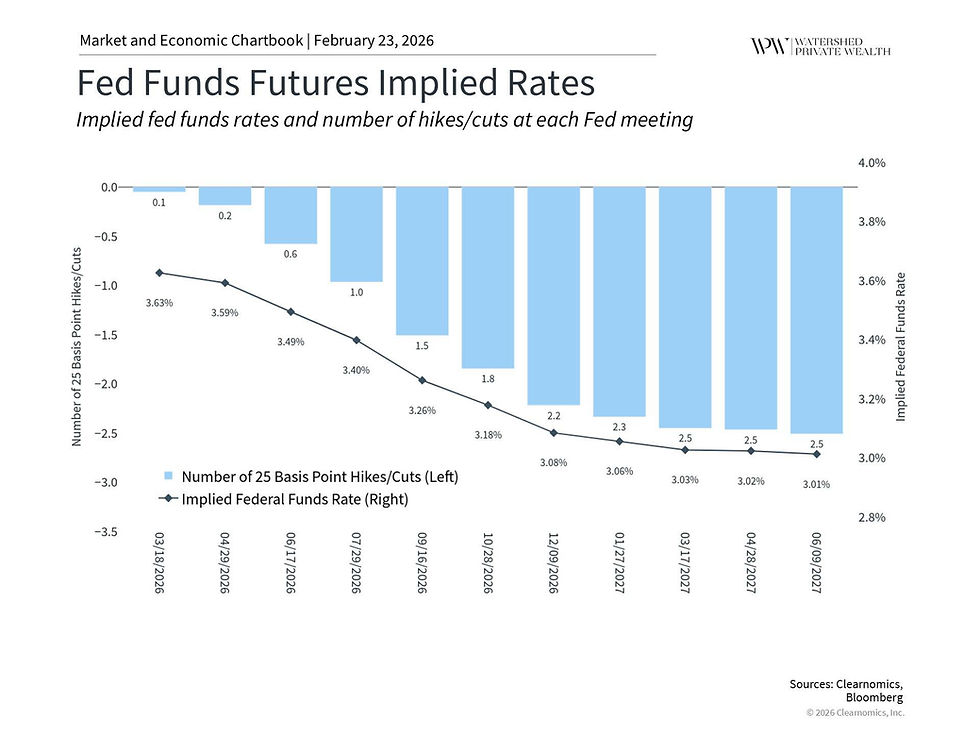

The broader picture for investors is cautiously positive — steady growth, easing inflation, and a cooling job market is about as balanced an environment as you can ask for. It supports both stocks and bonds, and keeps pressure off interest rates. The 10-year Treasury sits just above 4%, and markets expect at least two Fed rate cuts this year. Lower rates are good for portfolios; and even if rates hold steady, bonds are offering real returns and providing ballast when things get choppy.

The bottom line: the economy is healthy, the job market is cooling gradually, and the noise — tariffs, geopolitics, court rulings — is real but manageable. A balanced, long-term approach is still the right call.

Comments