The Bull Market: Good News Has Never Felt This Uncomfortable

- Joshi Koneru

- May 10

- 5 min read

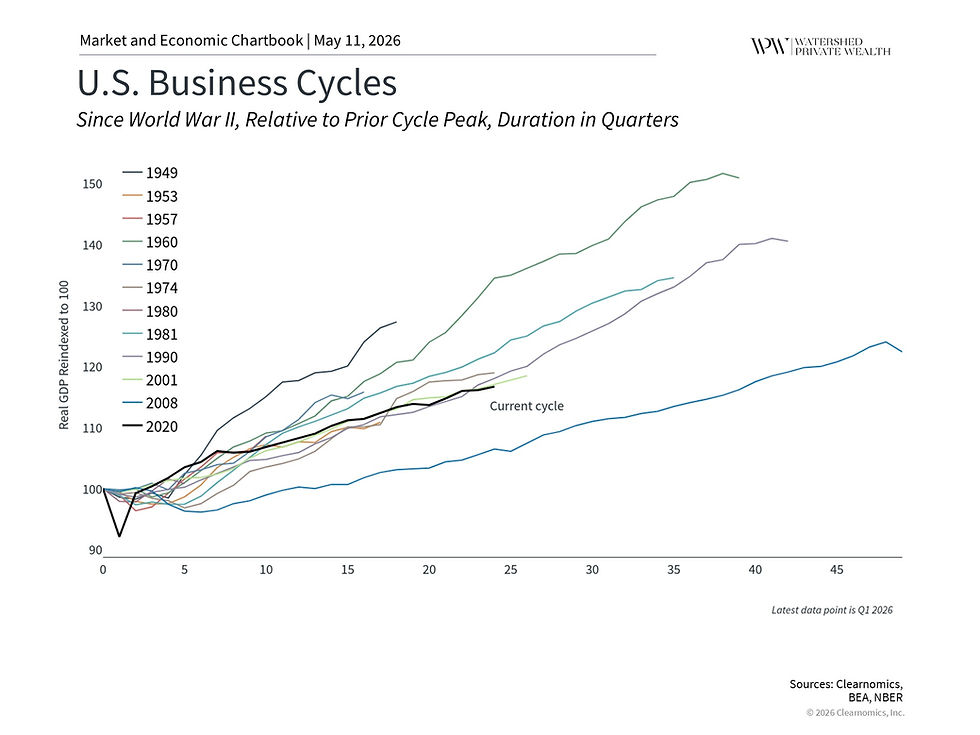

It has now been more than three and a half years since this bull market began in October 2022. Think about where we were: inflation was running at its fastest pace in fifty years, the Fed was hiking rates aggressively, and ChatGPT was still a month away from being unleashed on the world. Since then, the S&P 500 has more than doubled, and the Bloomberg U.S. Aggregate Bond index has fully recovered A lot has changed. What hasn't changed is the parade of market concerns making headlines. Every cycle brings new challenges and fresh doubts about whether the tried-and-true rules of investing still apply. And every cycle, those doubts are understandable. Each one is genuinely unique, with its own catalysts, innovations, and sources of uncertainty. But the underlying principles of investing and financial planning have stayed consistent across decades, and they have continued to point investors in the right direction this year. Bull markets climb a wall of worry  Geopolitics matter, but for long-term investors, the bigger picture is the market cycle itself. With the market near all-time highs, pullback anxiety is natural. The S&P 500 historically sees four or five pullbacks of 5% or worse every year. They are never fun, but overreacting to them tends to leave investors poorly positioned for what comes next. There is a reason investors say markets climb a "wall of worry." Over the past several years, that wall has included high inflation, a regional banking crisis, geopolitical conflicts, Fed policy fears, AI-driven concentration risk, and tariff volatility. None of those concerns were trivial. And yet, through all of them, the market kept climbing. The historical pattern is striking. Since World War II, bull markets have lasted far longer and produced far larger gains than what bear markets have taken away. Bear markets typically run one to two years. Recent bull markets have stretched ten years or longer. Even when corrections happen inside a bull market, the average decline is 14%, with the average recovery taking just four months. The bull market that followed the 2008 financial crisis lasted nearly eleven years and is still sometimes called "the most unloved bull market" because the worry never really stopped. In hindsight, those concerns, real as they were, never justified abandoning a long-term plan. Past performance is no guarantee, and recoveries depend on circumstances. But the historical record is consistent: reacting to every market move has, more often than not, meant missing most of the gains that followed. A growing economy is the foundation for long run returns  The stock market and the economy are not the same thing, but they are connected. Corporate earnings drive stock prices over the long run, and earnings depend on economic growth. That is why the broader economic cycle matters, even when markets are moving for entirely different reasons on any given day. The current business cycle has technically been running two and a half years longer than the market cycle. The last official recession was the brief but sharp pandemic contraction of 2020. Since then, there have been slower quarters and plenty of recession predictions, none of which have materialized. By most measures, the economy is still healthy. But there are three things investors are watching closely. Oil prices above $100 per barrel, if sustained, could weigh on consumer spending and reignite inflation. The job market has cooled, particularly in tech, which raises questions about whether the consumer spending strength of recent years can hold. And the scale of AI investment has prompted legitimate debate about whether we are in a bubble. That concern is understandable. Many investors today lived through both the dot-com bust and the housing crisis, so pattern recognition kicks in fast. Bubbles are notoriously hard to spot in real time, and not every stretch of high valuations ends in a dramatic collapse. What separates this cycle from past bubble concerns is that earnings growth has largely supported valuations, and many of the biggest AI spenders are doing so out of profits, not borrowed optimism. For long-term investors, the focus remains the same: stay balanced, capture the growth, and manage the risk. Stocks and bonds continue to work together  In 2022, when stocks and bonds fell at the same time, a lot of investors questioned whether bonds still had a role in a diversified portfolio. It was a fair question. The same doubt surfaced after 2008, when historically low interest rates made bonds look like dead weight. And yet, bonds have not only recovered, they are doing their job again. The Bloomberg U.S. Aggregate Bond Index has posted positive returns in each of the past two years, providing income and helping cushion equity volatility. International stocks and commodities have added to the diversification story as well. This is a familiar pattern. In the 1970s, inflation challenged the traditional portfolio. During the dotcom era, technology stocks became so dominant that everything else looked boring by comparison, right up until it didn't. In 2022, rising rates hit stocks and bonds simultaneously. Each period had its own version of "this time is different." Each time, the investors who stayed diversified and kept their eyes on the long game came out ahead. The headlines will keep coming. Markets will keep swinging. The bigger picture has not changed. The bottom line? More than three and a half years in, the principles have not changed. Stay balanced, stay focused, and let the market do what it has always done for patient investors. Footnotes 1. The number of pullbacks is based on S&P 500 index price returns since 1980. 2. The average size of corrections and recovery time are calculated from S&P 500 index total returns, since World War II. Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights. |

Comments